How a Tariff Fight Created the Federal Income Tax

Politicians quickly saw how much revenue the income tax could produce, so they abandoned its original purpose

By Phillip W. Magness

This article appears in the Winter 2026 issue of the Coolidge Review. Request a free copy of a future print issue.

The modern federal income tax arose in 1913 out of arguably commendable intentions, although they are not the intentions for which it is touted today. That year marked the ratification of the Sixteenth Amendment to the Constitution and President Woodrow Wilson’s signing of an accompanying implementation law, the Underwood Revenue Act.

Most modern accounts depict these events as a progressive triumph in the quest to rein in economic inequality. Thomas Piketty, a well-known socialist economist, calls “confiscatory taxation” an “American invention.” He credits it with putting an end to the Gilded Age and legitimizing a strong national power to redistribute earnings from the haves to the have-nots.

Although the federal income tax has certainly become a redistributive tool as well as a funder of the modern welfare state, these were not its original intentions. Indeed, it’s difficult to reconcile the details of the original American income tax with Piketty’s narrative.

What became the Sixteenth Amendment emerged out of a deeply conservative Congress four years earlier. It carried the endorsement of President William Howard Taft, generally regarded as a deficit hawk and opponent of government intervention in economic affairs. By modern standards, the Underwood Act’s income tax rates were minuscule. Most earners paid a tax rate of just 1 percent on income. The next-lowest bracket didn’t kick in until earnings exceeded $20,000 (about $650,000 today), and incomes beyond that threshold were taxed at just 2 percent. The highest rate applied only to the ultra-rich, taxing incomes above $500,000 (more than $16 million today) at just 7 percent. Few, if any, at the time viewed these percentages as onerous, let alone a serious foray into wide-scale redistribution.

But just five years later, President Wilson secured a massive tax hike. The top marginal rate rose to 77 percent, and all the other brackets saw large rate increases as well. The income tax system that emerged by the end of Wilson’s presidency laid the foundations for the income tax that we still have today—a steeply progressive tax that provides most federal funding.

This rapid transformation made the new income tax system unrecognizable to those who had helped secure the Sixteenth Amendment’s passage. One such figure was Joseph Weldon Bailey. As a Democrat representing Texas in the Senate, Bailey had begun the modern income tax movement with a speech he gave on April 15, 1909. After that speech, support for an income tax “flared up noticeably throughout the Nation,” according to future secretary of state Cordell Hull.

But by 1920, Bailey had disavowed his creation. The income tax had become “a tax to penalize prosperity,” he said, an indecipherable riddle of accounting that “could not be understood by the congressmen themselves.” Bailey explained, “A law which takes from one class to give to another class is essentially Socialistic.”

By turning back to the events of 1909 to 1913, we discover that the income tax’s history is shrouded in progressive mythology.

A Club to Beat Down Tariffs

The proposal that became the Sixteenth Amendment originated in the middle of a now-obscure debate over tariffs, which then supplied the majority of the federal government’s tax revenue. In 1909, President Taft tasked Congress with modernizing the federal tariff schedule to improve its tax yield and guard against budget deficits. Senator Nelson W. Aldrich, an arch-protectionist Republican from Rhode Island, seized the occasion to produce the Payne-Aldrich Tariff bill. This pork-laden measure rewarded politically connected industries with favorable rates while penalizing their competitors abroad.

Lacking the votes to defeat Aldrich’s tariff head-on, Bailey came up with an innovative flanking maneuver. Taking to the Senate floor in April, he explained, “I would provide for the reduction of the duties on articles of common necessity, and then I would supply the deficiency of revenue created by a remission of those duties to the people by the levy of an income tax.” If this income tax passed as a rider to the tariff bill, Aldrich could no longer hide his protectionist favors to lobbyists behind the pretext of raising revenue.

Aldrich recognized the ploy and countered his Democratic colleague: “Perhaps you would like to reduce the revenues for the purpose of imposing an income tax and thus taking the first steps for the destruction of the protective system.”

Bailey’s flanking maneuver split the chamber. A small group of Republican “insurgent” senators, frustrated with Aldrich’s overreach, offered to back Bailey’s proposal or a similar measure of their own sponsored by Albert Cummins of Iowa. After three weeks of vote counting behind the scenes, Aldrich realized that he remained three votes short of being able to pass a “clean” version of his tariff schedule, without Bailey’s income tax swap. To salvage his tariff, he tabled the bill for a month and begged President Taft to intervene with wayward Republicans.

Aldrich and Taft reportedly discussed the tariff issue during leisure rides around Washington in the president’s new motorcar. Although the details of those conversations are lost to history, Taft recounted Aldrich’s conundrum in a lengthy letter to his brother. Bailey, he revealed, had “secured the assent of nineteen Republicans in addition to all of the Democrats to . . . pass a regular income tax.” If Aldrich reopened the tariff bill, he would probably lose.

But Bailey faced a challenge of his own, Taft noted. Even if the income tax rider passed, it would go “exactly in the teeth of the decision of the Supreme Court.” In the 1895 case Pollock v. Farmers’ Loan and Trust, the U.S. Supreme Court had struck down an earlier tax on income derived from interest, dividends, and rents. The court held that these measures constituted a “direct tax” and, as such, fell under a complex census apportionment restriction in the Constitution. Although Bailey’s rider carefully designated his new income tax as an “excise” on earnings, his measure would almost certainly face a protracted court battle.

Taft brokered a compromise. He convinced Aldrich to pursue a constitutional amendment to legitimize the income tax, thus avoiding a Supreme Court challenge. Along with a few minor tax concessions, this measure proved sufficient to peel some insurgent votes away and keep the Payne-Aldrich Tariff intact. The proposed amendment stripped the income tax supporters of their urgency, pushing any bill down the road by several years. Aldrich felt confident that an income tax amendment would not win ratification.

Though outmaneuvered on the tariff issue, Bailey became a champion of the new constitutional amendment and toured state capitols to urge its ratification. Its main appeal lay not in progressive redistribution or even in enabling more government spending. Rather, as one Georgia legislator put it during the ratification fight, the amendment would provide “a club to beat down [the] high protective tariff.”

This tax-swap strategy had been circulating in academic discussions for years. It originated not with socialist or labor agitation but with the laissez-faire economist William Graham Sumner, who floated the idea in 1878. “If we had an income tax and could do away with tariff taxes,” Sumner said, we could break the special interest capture of federal tax policy. Amid the ratification debate, Davis Dewey, chair of the economics department at MIT, reiterated this rationale. The Sixteenth Amendment would “divorce this alliance” between “taxes and industrial enterprise” and thus “lessen the importance of the tariff system of import duties.”

Wilson: End “Artificial Advantage”

The amendment cleared its ratification threshold on February 3, 1913, when Delaware gave its consent. Two months later, the newly inaugurated president, Woodrow Wilson, approached Congress to overhaul the federal tax system.

Notably, Wilson did not emphasize redistribution or even the income tax component of the newly introduced Underwood Revenue Bill. First and foremost, the president wanted tariff reform. “Consciously or unconsciously, we have built up a set of privileges and exemptions from competition” through protective tariffs for politically connected industries. His charge for reform was simple: “We must abolish everything that bears even the semblance of privilege or of any kind of artificial advantage, and put our business men and producers under the stimulation” of the market. Wilson continued: “The object of the tariff duties henceforth laid must be effective competition, the whetting of American wits by contest with the wits of the rest of the world.”

The Underwood bill dismantled Aldrich’s beloved tariff schedule, although the Rhode Island senator was no longer around to defend it. After thirty years in the Senate, he had retired in 1911 owing to declining health. In 1912 an electoral wave, fueled in part by popular backlash against the Payne-Aldrich Tariff’s excesses, handed Democrats control of both chambers of Congress. The new revenue bill phased in tariff reductions, lowering rates from an average of 40 percent in 1913 to just 16 percent by 1920. To offset tariff revenue losses, it executed the tax swap from Bailey’s earlier proposal. The United States added a modest new income tax.

The Birth of Confiscatory Taxation

How did this limited tariff-replacement measure become the pillar of the federal tax system we know today? The answer lies in its revenue-generating prowess, not for redistribution but rather for warfare.

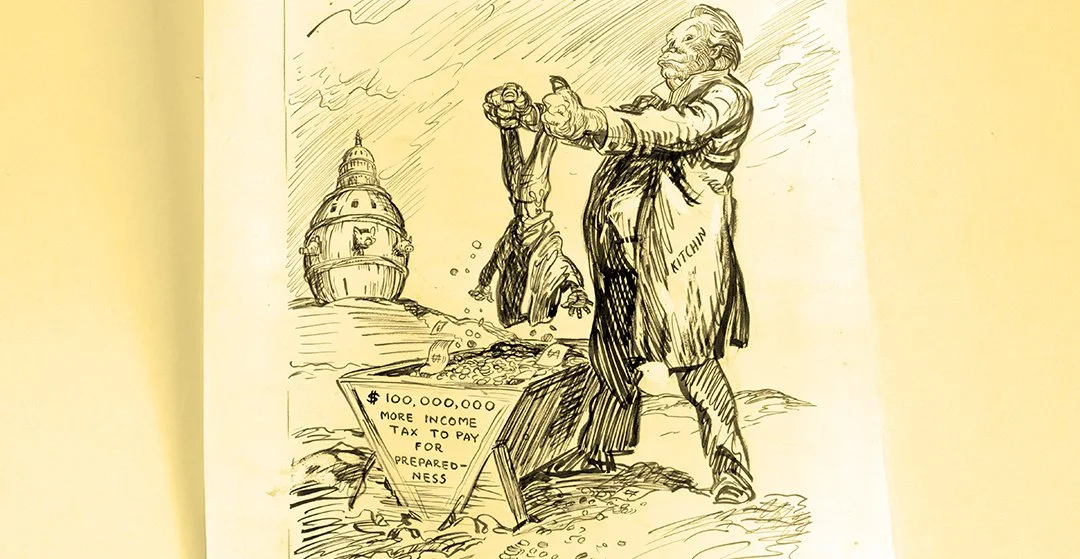

After winning reelection in 1916, President Wilson increased military expenditures in preparation for possible U.S. entry into the Great War. A new Revenue Act passed in September 1916 ratcheted the top income tax bracket to 15 percent, a sizable increase but still modest by today’s standards. The next year, after the United States officially entered the war, Wilson secured another tax hike, bumping the top bracket up to 20 percent. The largest increase came from yet another measure in 1918, which set the infamous 77 percent top marginal rate.

The rate hike stunned even veteran advocates of income taxation. Columbia University professor Edwin R. A. Seligman, who had published a 750-page academic treatise in support of the Sixteenth Amendment in 1911, struggled to comprehend Wilson’s move: “Never before, in the annals of civilization, has an attempt been made to take as much as two-thirds of a man’s income by taxation.” And yet military exigency demanded it.

To secure this measure, Wilson again asked Congress to supply “adequate resources for the Treasury for the conduct of the war.” Reviewing his previous tax hike, the president reported that “the four billions now provided for by taxation will not of themselves sustain the greatly enlarged budget to which we must immediately look forward.” He said that “only fair, equitably distributed taxation of the widest incidence” would fulfill this job.

The rich were to be taxed at extravagant rates not because of their means but because, Wilson claimed, their incomes benefited the most from the industrial mobilization demanded by war. Indeed, in Wilson’s telling, taxation became synonymous with patriotism and the American military cause: “Our financial program must no more be left in doubt or suffered to lag than our ordnance program or our ship program or our munitions program, or our program for making millions of men ready.”

No Turning Back

The resumption of peace provided an occasion for income tax reductions in 1921, 1924, and 1926 under successive Republican administrations and Congresses. Although these measures brought the top rates back to earth, settling at 25 percent when all was finished, the United States never again approached the restrained income tax system from the original tariff reform efforts of 1913.

Income taxation yielded more revenue than anyone imagined at its origin, and politicians like having money to spend.

Phillip W. Magness is the David J. Theroux Chair in Political Economy at the Independent Institute.

This article appears in the Winter 2026 issue of the Coolidge Review. Request a free copy of a future print issue.